The Office for Budget Responsibility downgraded its growth forecast for 2019 yesterday from 1.6% to 1.2%, in line with the Chancellor’s Spring Statement.

The OBR pointed to the global slowdown and a degree of knock-on effect from Brexit as causes for the economic slowdown but highlighted a much better performance over the next five years.

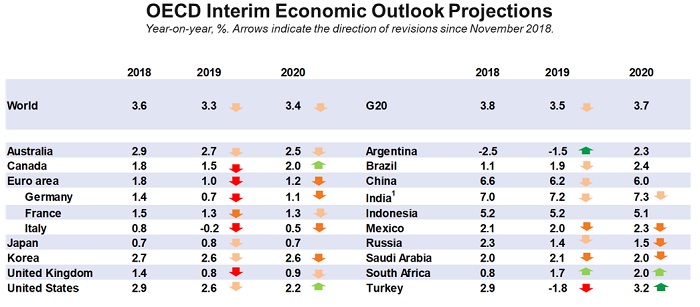

The data comes only days after the Organisation for Economic Co-operation and Development (OECD) reported that UK growth would be much worse off for the Brexit uncertainty; down at 0.7% growth this year from 1.4%.

.

.

The Office for Budget Responsibility also reported that the UK government faced a shortfall in income, despite savings made by Philip Hammond’s department. The forecast points to UK house prices falling in 2019, and the OBR expects negative inflation before a return to normality in 2021. The shortfall is estimated at around £3 billion in stamp duty tax receipts; a figure which will join another £2 billion shortfall in corporate tax payments due to firms leaving the UK.

The governments saving grave is that improved income tax and national insurance contributions should keep the UK’s annual deficit at 0.5% of GDP, and in the process reduce debt from the current 83.3% of GDP to 73% by 2023-24. Arguments have been made against the savings, with the Resolution Foundation stating that cuts to public services are forcing austerity on the public.

The Pound has risen today following last night’s Commons vote against a no-deal Brexit, with investors slightly optimistic about the idea of Britain avoiding the worst case scenario exit. Sterling peaked at $1.3380 at around 9pm last night – the highest it has been since last June – and slowly fell back before peaking at $1.33 again in the early hours of this morning. The Pound also rose to a 22-month high of €1.18 in the process.

Edwin Morgan, interim Director General of the Institute of Directors, is one business leader who is less than happy with the current situation.

“After more than two years of repeated disappointments, business leaders once again find themselves at the mercy of politicians, hoping that compromise will finally win out. For far too long the real interests and concerns of employers and their staff have played second fiddle to the political psychodrama that our trading partners and competitors have been watching with bemusement.”

Today’s vote in Parliament will decide whether or not to extend Article 50 and delay Brexit, something many MPs and journalists think is almost a certainty to happen. On Monday, Catherine McGuinness (Policy Chair at the City of London Corporation) warned: “Extending Article 50 would be one way of avoiding the UK crashing out of the European Union without a deal but this would only be a sticking plaster unless the deep, underlying issues are resolved. Politicians must use any extension to work together as a matter of urgency to secure a deal, locking in a legally binding transition within the necessary timeframe.”

The House will begin discussions from 12:30pm today, until around 7pm this evening, after which MPs will proceed toward voting on the government’s motion on Article 50, as well as any amendments approved for vote by the Speaker of the House, John Bercow. Should amendments pass then the original motion will be amended, ready for the final vote.

.