In the continuing effort to try and minimise the economic impact of Covid-19 on the global economy, many nations are increasing national debt to pump liquidity into struggling markets. While these measures are understandable, they have raised fears for many analysts of a potentially catastrophic debt default to come in the next few years.

The US and EU have both embarked on significant fiscal stimulus programs, in a bid to keep their economies afloat during one of the most significant crises of modern history. Indeed, the lockdowns of March, April and May represent an industrial shutdown on a scale never before seen.

At a time when economic output has been significantly reduced, governments have also borne the cost of paying wages for many workers to stop unemployment from rising even higher than it already has. This unprecedented action however has unbalanced national spending, and increased debt significantly, with worrying potential results.

The EU is relaxing rules on bank borrowing, while at same time injecting huge liquidity into its economy due to the pandemic, and borrowing to fund it. The danger of this cycle is banks borrowing from the ECB and then using the funds to buy bonds, which are essentially national debt anyway. This risks creating what has been named the “doom loop”, as seen in the 2012 EU crisis.

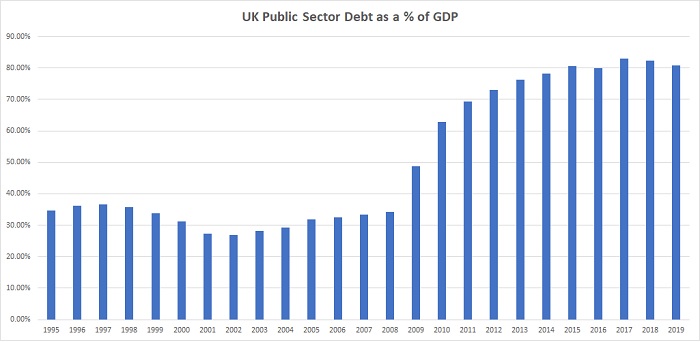

The Bank of England has released £745 billion of liquidity into the UK economy through its bond buying QE programs since 2008, and now owns more than 30% of national debt. The UK government has borrowed a record £55.2 billion in May alone, and this creates a similarly dangerous risk of a ‘doom loop’ for the UK in the years to come.

As seen in the chart above, UK debt had been rising consistently since the last financial crisis, and the coronavirus could be the straw that breaks the camel’s back.

In the US, debt has climbed to $26 trillion due to the pandemic. This has seen their deficit hit $1.8 trillion for just Q1 of 2020 – nearly double the entire deficit for 2019 – and Q2 is expected to be worse.

This increasing debt burden on the US economy, especially with output likely to shrink during 2020 at least, increases the risk of a US debt default. If this were to happen, the damage to the global economy would be difficult to overstate. Interest rates would rise significantly, while the Dollar would drop in value. This would cause inflation, and very likely hyperinflation. This hyperinflation would lead to a very deep recession, and a lack of government funds to pay federal salaries and pensions.

Whether the US has ever experienced a true debt default is a topic of debate, but Iceland does provide a clear example of what a debt default can do. When Iceland defaulted in 2009, it caused their national currency – the Krona – to drop 50% in just one week, while inflation soared to 18.16%. With the Dollar so firmly rooted into the financial dealings of the world, a US debt default would inevitably have a far greater impact that could prove catastrophic for the global economy.

With the outcome of the coronavirus still largely unclear, debt could continue to grow for years to come, and the more borrowed, the higher the risk of a default. Governments will have to very carefully balance these risks, against taking significant measures to try and reduce their debt burdens as soon as possible. With uncertainty so high, many investors are choosing to add precious metals to their portfolios to protect their wealth in the event a debt default does occur.