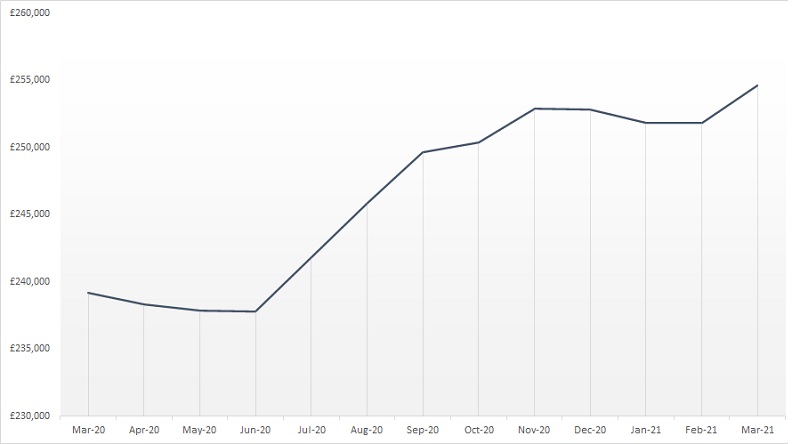

Average house prices have reached a new record high in March, despite the ongoing economic uncertainty caused by the Covid-19 pandemic. House prices climbed to an average of £254,606 based on figures from Halifax and their House Price Index report.

The rise in prices represents an increase of 1.1% on February alone, and means the average house now costs 6.5% more (around £15,000) than March 2020 when the pandemic began.

Average house price in the past 12 months. Figures from the Halifax House Price Index.

The rise in house prices during economic downturn are considered somewhat surprising, given increasing unemployment, and many people seeing reduced wages while on furlough. As Russell Galley, Managing Director at Halifax, put it: “Casting our minds back 12 months, few could have predicted quite how well the housing market would ride out the impact of the pandemic so far, let alone post growth of more than £1,000 per month on average.”

Analysts expect for the strength in the housing market to continue for the next few months, based on the current and ongoing factors boosting prices, but warn that the gains could tail off after that, while others believe the market could be something of a bubble given the economic situation facing the UK.

A number of measures have been introduced by the government in the past 12 months with the intention of keeping the housing market healthy. The stamp duty holiday has helped keep movers in the market, while the new 95% mortgage guarantee scheme will be encouraging some first-time buyers to take the plunge.

While the past year has seen many people made redundant or living on reduced wages during furlough, those who have remained working full time have also spent less during prolonged periods of lockdown. The Bank of England estimates that £100bn has been built up by UK savers during this time, money which for some will almost certainly be used towards property.

Many of these boosting factors for the housing market do have an end in sight however; the stamp duty holiday is due to end by September, with furlough ending at the same time. Office worker’s mass exodus from cities have also boosted prices in more rural areas, but as restrictions end the landscape for homeworking could revert towards a hybrid model or full-time office work, that could see this trend reverse once more as people move closer to work.

While the housing market is in some ways enjoying a pandemic boost, this could therefore grind to a halt towards the end of the year, and analysts are quick to caution there could be price falls to come following March’s new record.

The ongoing house shortage should help mitigate any potential price drops in the coming months, and as with many other parts of the global economy, inflation is beginning to be of concern for house builders. Shortages of essential materials have seen some price rises here in the UK as well as globally. In the US, lumber prices have risen by over 108% since last April, adding significant costs to house builders.

The housing market has in some ways then performed similarly to the stock market, reaching new highs in seeming contrast to the reality of the global economy. The dearth of houses for sale, and potential rising costs on new builds could help buffer any potential bubble, but with government support ending in the second half of the year the housing market could face challenges following years of growth.