Evidence of inflation is continuing to mount, as the UK consumer price index – CPI – climbed to 2.1% in May. This puts UK inflation at its highest in two years, and above the Bank of England’s target of 2%.

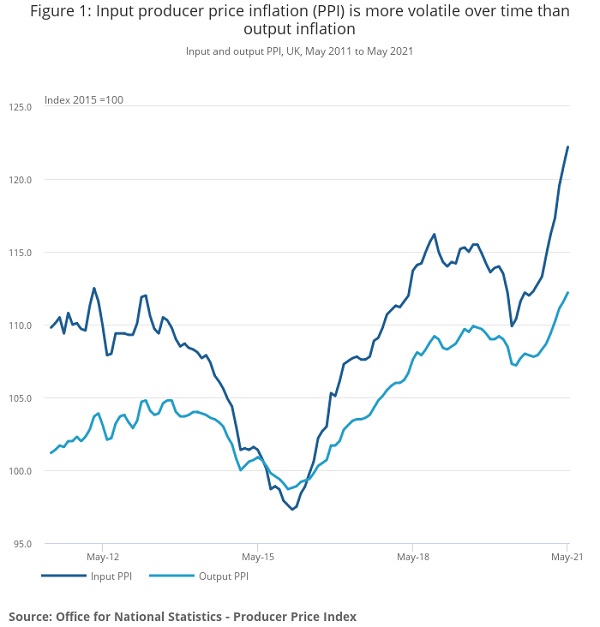

Manufacturing inflation also shows worrying signs of further rises to come. Input costs to Britain’s factories rose by a worrying 10.7% year-on-year, the highest rise since September 2011. The rise in costs came as key materials like copper soared in May. For now, manufacturers have taken on some of the additional cost, but still increased their prices by 4.6% year-on-year.

Food, clothing, game downloads, and motor fuels all contributed to the larger than expected rise in CPI. Even core CPI however, which removes more volatile contributors like food and energy, was still 2%, above market expectations and already hitting the BoE target.

As has been the dominating theme of the past few months however, markets are debating on whether this is the beginning of a problematic period of high inflation, or a transitory spike as restrictions are eased following 2020s strict lockdowns globally.

Materials like lumber and copper have pulled back following their recent surge, which could help reduce costs for manufacturers. Oil prices are rising however and are up nearly 50% so far in 2021, the shortage of semiconductors also rages on, suggesting there may be ongoing supply issues and increased costs for manufacturers still to come in the months ahead.

Analysts are unsurprisingly split on the transitory question. Jack Leslie, Senior Economist at the Resolution Foundry summed it up thusly – “Longer term, for inflation to become a concern we would need to see a sustained increase as a result of rising inflation expectations (rather than a temporary one as lockdowns ease around the world). There's not any evidence that is happening yet in the UK.”

Others are concerned however that inflation could become connected to wage rises. Some employers are struggling to hire enough staff amidst the risks of the pandemic, with minimum wage failing to entice workers in an increasingly expensive world. KPMG UK’s Chief Economist Yael Selfin said that “There is a greater level of uncertainty about prices at present, with a possibility that inflation will turn out to be higher if staff shortages persist, triggering stronger wage rises, while cost increases continue to be passed on to consumers.”

Markets so far have largely shrugged off the recent inflation rises in the US and UK, accepting the transitory argument so far. This has seen gold pull back from $1,900 to around $1,860 per ounce this week. Gold is caught between both the wait for some sign of long-term inflation, and the potential increase of interest rates when central banks begin to taper economic support.

In the UK, today's data has given Sterling a small boost. Renewed difficulties over the Brexit withdrawal agreement, and the announcement of a four-week delay to the end of Covid restrictions had pushed the Pound down to a monthly low of $1.403 yesterday. The inflation increase however has once again spurred speculation the BoE may raise interest rates sooner than expected, and Sterling has risen to $1.411 today.

This has seen gold fall 1.2% on the week, to around £1,318 per ounce in trading today. Silver meanwhile has enjoyed a better performance in the same period as industrial production and investment popularity keeps demand high. Silver is up 1.12% on the week and is trading at £19.70 per ounce.

With the US Federal Reserve holding a key meeting today, markets are watching closely for any signs of tapering across the Atlantic. The consensus however is that the Fed will stick to the transitory message for now, with perhaps the slightest mention that they are thinking of thinking about tapering at best.