In what has already been a chaotic week for the UK financial market, the Bank of England has today taken the unusual step of intervening to prop up UK bonds. The BoE called rising bond yields a “material risk to UK financial stability” in what will undoubtedly be a blow to new PM Liz Truss and her Chancellor.

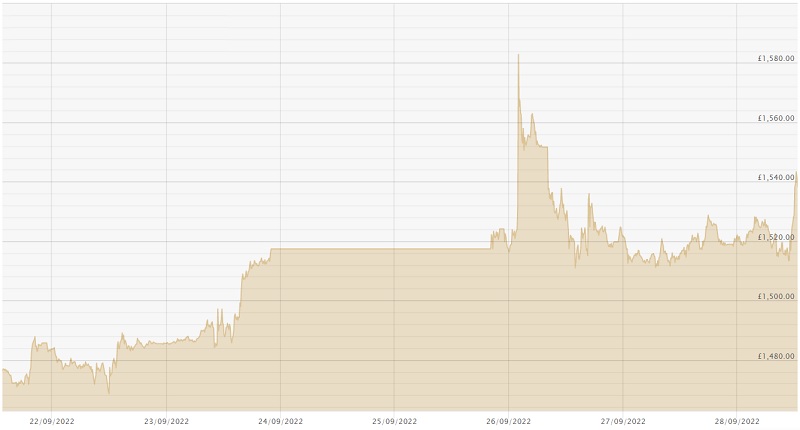

The gold price in GBP this week. Highly volatile including a new UK record.

Following on from last week’s mini budget from the new government, Monday saw the pound fall to an all-time low of $1.0327 against the dollar. Markets were firmly against the unfunded bumper tax cuts being offered by the Conservatives, and the risks they posed to growing UK debt. Analysts and institutions including the IMF warned of the risks posed by a government cutting taxes and borrowing to do so, whilst also trying to bring inflation back under control.

Sterling had recovered somewhat on expectations that either the government would be forced to U-turn on some of the announced cuts, or that the BoE would announce an emergency interest rate hike to try and stabilise the pound. With neither event looking likely however the pound had continued to struggle, and UK bonds saw yields rising to their highest since the financial crisis.

With UK debt set to grow under the government’s plans, these higher yields risked even higher repayments years down the line, and had seen UK debt lagging behind that of Italy and Greece. Pension providers in particular were reporting issues with margin calls on their liabilities, and were a big part of the BoE’s intervention.

The Bank announced earlier today that it would pause the planned sale of bonds, and would instead resume buying them in order to help stabilise the bond market. This means the BoE is now resuming Quantitative Easing almost immediately after ending it. The plans have helped bring bond yields down for now, but have seen the pound slump once more, hitting $1.0571 at its lowest.

This of course does little to help the root problem causing Sterling’s collapse. The Bank of England are raising interest rates in the hopes of slowing demand and growth, bringing inflation back down to their 2% target. The UK government however are aiming for higher demand and growth by lowering taxes. The analogy of one foot on the brake, and one on the accelerator has been widely used in response to last week’s budget, and markets clearly feel the same.

The BoE isn’t set to have another committee meeting until early November, and so far, seem reluctant to hold an emergency meeting over interest rates. If they do make it to November’s meeting, a much more aggressive hike is expected in order to try and bring some strength back into the pound.

Forecasts suggest interest rates could double to 6% by next summer, prompting fears of a house market crash as owner’s default on rising mortgage repayments, or struggle to secure mortgages in the first place. The Chancellor has attempted to placate markets with a promised full policy plan to be laid out in November, but markets are clearly unimpressed, and unwilling to invest in UK debt long-term.

The collapse in Sterling saw gold briefly hit a new all-time high here in the UK on Monday, at £1,582.87, and remains high today, trading at around £1,540 per ounce so far. Demand for precious metals has risen significant in the past two weeks as investors look for safer places to park their savings than Sterling or bonds. Volatility is expected to continue until the government or BoE step up to the plate, and all eyes on will be on GBP for any signs of hitting parity with the dollar.