Core inflation for the UK has hit a 30-year high this morning, as prices continue to rise. Today’s figures will cause more headaches for the Bank of England and will almost certainly spur further interest rate hikes in the months ahead.

Although the CPI rate fell from 10.7% to 8.7% annually, this was still above market expectations, and was largely due to energy prices, which have now caught up with April 2022, when they soared by 50%. Alcohol, tobacco, and communications were some of the largest drivers of inflation, but food prices also remain high, increasing by a worrying 19% in April alone.

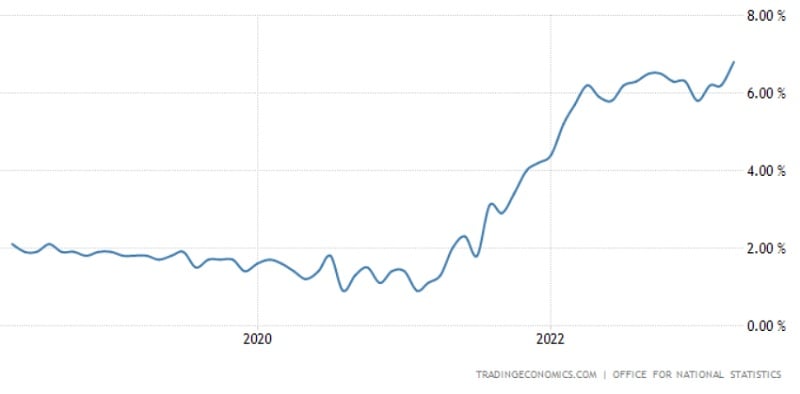

Chart showing the UK’s core inflation rate. Chart from Trading Economics.

More worryingly for the BoE however was core inflation, which continued to rise from 6.2% last month to 6.8%. This is the highest core inflation has been since 1992 and will add further pressure to the BoE to bring inflation down. Markets have now priced-in a 100% chance that the BoE will hike interest rates again to 4.75% in June.

Further hikes beyond this are also expected, markets now believe rates will climb to 5% and above over the summer and remain high well into 2024. After years of low interest rates, it’s uncertain how well the UK economy will cope with higher rates. UK mortgage holders in particular could face significant increases to their monthly repayments that could have a profound impact on house prices in the months to come.

Mortgage activity in the UK has already shown signs of slowing, as buyers are put off by higher borrowing costs. House prices have already stalled following strong growth, particularly during the past three years, and have fallen in some areas. If buyers continue to dry up, and some homeowners are forced to downsize to make their mortgages more affordable, this could see house price slashed in the months ahead.

The Bank of England then will have little choice but to continue hiking for at least one more meeting given how sticky core inflation is proving to be, but they will be all too aware of the risk they could cause a housing market crash. News that Skipton Building Society are launching a no-deposit 100% mortgage also calls back to the financial crisis of 2007, caused by similar subprime mortgage debt.

Despite an optimistic revision to the UK’s economic outlook from the IMF yesterday, there looks to be plenty under the hood for investors to be wary of in the months ahead.