A volatile mix of economic and geopolitical factors has caused large price swings for gold and silver this week.

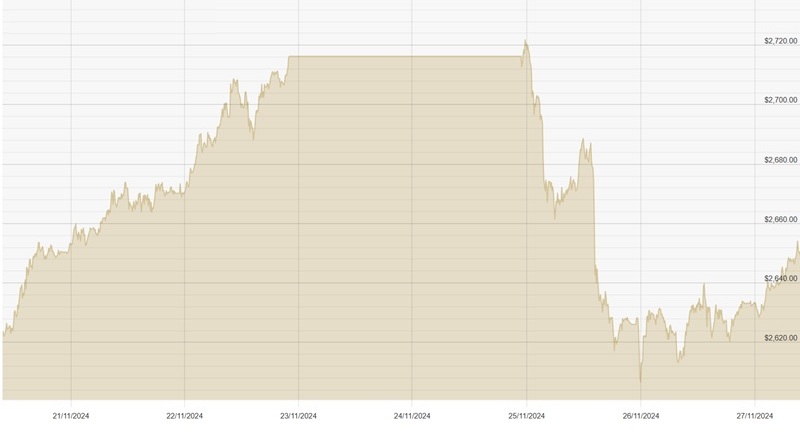

After climbing to a new all-time high in many currencies over the weekend, gold dropped sharply on the market open and into Monday, wiping out almost all of the gains. Gold has found some support however, and has regained $2,650/£2,100/€2,500 at the time of writing.

‘No news is good news’ seems to be the mindset on Ukraine in the past few days, and despite no signs of de-escalation, a lack of headlines over the weekend and hopes of a deal when Trump takes office in January have calmed markets for now. Any news of further escalation however could see safe haven buying return and push gold higher.

A ceasefire between Israel and Hezbollah in Lebanon has also been agreed, and will be seen as a welcome first sign of some stability in the Middle East.

Also weighing on gold was confirmation from Donald Trump that tariffs would be placed on goods from Canada, China, and Mexico at the start of his second term. The news put pressure on stock markets, and saw the dollar strengthen. Tariffs would drive prices higher in the US, increasing inflation, and reducing the Federal Reserve’s capacity for cutting interest rates.

A trade war will only worsen the current fragile global economy however, and will add to the risks already faced in many countries. The price of silver also slipped from over $31 to a low of $30.07 on Monday morning, and will likely be more severely impacted by any potential trade wars reducing its industrial demand.

A 6% gain for gold in a week, followed by a 5% drop when the market opens is certainly unusual, and reflects the degree of uncertainty around the world. Further jumps and dips are likely in the next few weeks, and surrounding the inauguration of Donald Trump in January. The general trend for gold remains extremely positive however, with the metal up more than 30% in the past 12 months.