Gold and silver prices have stabilised after a sharp sell-off prompted by the ceasefire between Israel and Iran.

After a shaky start, the ceasefire between the two countries appears to be holding for now at least, and markets have calmed after a volatile 12 days.

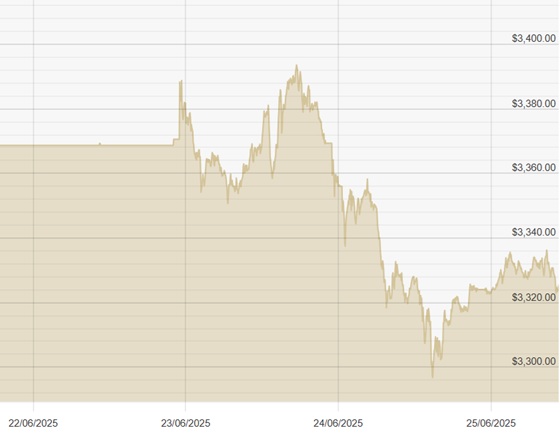

Gold fell from $3,391 on Monday to a low of $3,296 yesterday, but has recovered some of the losses, trading at $3,327 at the time of writing. In GBP, gold fell below £2,500 to as low as £2,421 but is now back to £2,443. In Euros, gold has dropped below €2,900 but is holding around €2,869.

Silver was less impacted by the Middle East news, and had already seen prices fall from $37.31 last week to $36 at the weekend close. Silver did dip as low as $35.34 yesterday, but found support above the key $35 level once more, and has bounced back to $35.89 this morning.

The ceasefire was something of a surprise to markets, and came after several days of escalation, including a strike by the US against Iranian nuclear sites. Both countries have acknowledged the ceasefire, though a leaked report from the Pentagon suggests the US strikes may not have been as effective as claimed by President Trump. The price of oil has dropped as markets hope that the ceasefire marks an end to the conflict, but it remains to be seen whether Israel and Iran will stick to it.

With gold still above $3,300 per ounce it remains at historically high levels. The ’12-Day War’, as the conflict between Israel and Iran has been dubbed by Trump, was only a brief bump to the metal price, and only added to the fundamentals that have driven gold higher in the past 12 months.

If the conflict has truly ended, then markets will simply turn back to the trade war, growing US debt, and persistent inflation, all of which continue to support gold.