The gold : silver ratio has surged to record highs in recent weeks, as a slump in industrial demand holds back the alternative investment metal.

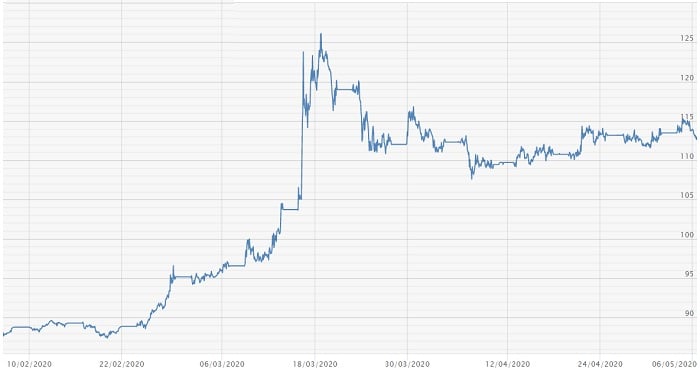

The ratio, seen as a key indicator by many investors, hit an all-time high of 126 in March as the coronavirus pandemic spread across the globe, and shutdowns across Europe and America began. This has dropped to 115 at present, higher than the average of 90 for 2019, and far above the 60 – 70 considered the normal baseline. This means that currently for the price of one ounce of gold, 115 ounces of silver could be purchased.

The gold : silver ratio for the past three months, showing a sharp rise as the global pandemic worsened across March.

Gold has gained 13.8% in value in the past three months, as the pandemic prompted a surge in investor demand, and drove the price up to records in Sterling and Euros. Although silver has seen a similar (if not greater) surge in demand from investors, it’s value has actually fallen by 11.5% in the same three month period, causing the gold : silver ratio to increase.

The disparity between the two metals then during this crisis has led some to question why the silver price has dropped while gold has been enjoying such an increase. The main reason for this is that silver is much more reliant on industrial demand (accounting for about 60% of global silver consumption), with investment bullion only accounting for about 20% of silver consumption. This is versus industrial consumption standing at about just 9% for gold, versus 25% for investment bullion, making gold far less dependent on its use in electronics.

February and March saw most of the world’s biggest manufacturers (such as Apple and Samsung) close their production facilities, as the virus spread across Asia. Although some have begun to reopen, these companies now face closed retail outlets across Europe and America, reducing any demand for their products if they do make them. As such, these companies have not been ordering the tonnes of silver they would normally need for the electronics in their products, and no amount of investment demand has been able to make up for this shortfall.

Although consumer demand for bullion has surged, many refiners across Europe have also had to close their facilities temporarily due to the lockdowns in their respective countries. This will have further reduced the wholesale orders for silver, and weakened the price, despite investors clamouring for any silver bars and silver coins they can get.

At the time of the ratio peak of 126, mines in South Africa and South America remained open, and supply was strong with limited demand, causing the silver price to drop. April saw cases spread across the world, and some mines have since closed, or reduced operational capacity to safeguard employees, and could hint at a future supply shortage to come for silver.

Silver has long been considered undervalued, and as manufacturing resumes, and the lockdowns end in the coming weeks and months, silver could enjoy a surge that will see it close the gap on gold.

When factories begin full production once more, they will all likely need to place large orders for silver, and some may even place larger than normal orders while the price is so low, and with the shipping disruption of recent weeks fresh in their minds. This will likely coincide with bullion refiners resuming their own operations and placing large orders to meet the sudden investor demand for silver.

If this overlaps with any potential supply shortages to come as a result of the suspension of mining operations, then the supply and demand paradigm that dropped silver’s price in March could flip and push silver back towards its peaks of the 2008 financial crisis, in the way gold has been.