Gold vs Buy-to-Let

For years, having a rental property has been considered a smart way to make large investments. A tangible asset, steady monthly income, and a large profit upon sale are all draws that seem like a no-brainer for an investor. In recent years though, changes to regulations combined with market uncertainty have diminished the potential returns for buy-to-let properties significantly. Managed poorly you could even see your investment lose money.

Buying a rental property

The first major hurdle is funding a buy-to-let property. The average house price in March 2023 was £285,009 (Source: ONS). Unless you have the capital already, this would be a sizeable figure to overcome for most investors. With prior funds/inheritance you can reduce the cost of purchasing a second property, but if you don’t have these funds available then you’ll need to look at raising the money through borrowing.

A residential mortgage can already be an expensive prospect but, when purchasing a property for rental purposes, you’ll need to apply for a buy-to-let mortgage. Due to the risks involved with renting out a property, a buy-to-let mortgage has much stricter and expensive restrictions placed on them.

A buy-to-let mortgage will typically require a much higher deposit than a residential one. This can be 25% or higher, and in our example average house this would result in paying a deposit of £71,252.25, still out of reach for many investors. Interest rates can also be higher for a buy-to-let mortgage, but this may be offset by the reduced loan-to-value ratio. Rates have soared however in recent months, as the Bank of England hikes interest rates to combat high inflation. As such, typical buy-to-let mortgage rates have gone above 6% at the time of writing, and represent a significant challenge for any investor considering borrowing to finance a property investment, or those needing to refinance.

A mortgage is leverage but there is added risk involved in taking on debt to invest. A 5% shift either way on a £100,000 property is a greater swing of value than 5% affecting £10,000 worth of gold bullion. This is great if market prices improve, but if house prices should fall (as they are forecast to in the coming months) then you could find your asset has decreased in value.

It’s important to remember that a mortgage will not be your only cost when purchasing the property. Legal fees, agency fees, and surveys will be required. Since 2016, Stamp Duty on a second home/buy-to-let property has a surcharge of an additional 3% per tax bracket. For our example home this would mean paying an additional £10,300 of tax just for purchasing it.

Lastly, it is important not to underestimate the impact of refurbishing the property. Most people when looking for a rental property expect a high quality of finish, as well as furnishings. A new kitchen with white goods, a new bathroom, carpeting the property… all of this could easily add more than £50,000 cost to the project and result in the property being empty while work is completed.

With a huge initial cost, and large monthly mortgage payments to make, you need your rental income to cover this cost and ideally surpass it, but this is not always possible.

Cost of a rental property

The property is yours, it has been refurbished, and after a few months of viewings you have found a tenant. It is easy to imagine that you can sit back and let the money roll in. If you have a mortgage repayment of £1000 pcm and you’re renting the property out at £1350 pcm then it might seem like your yield is £350. The reality however is that there is a myriad of hidden costs that could easily reduce this yield to little or nothing, or worse – even a loss.

Landlord Insurance is a smart way to protect your investment, though not compulsory. If tenants cause damage to the property then Landlord Insurance could save you from costly repairs and the purchase of new furnishings. As with any non-compulsory insurance it is a gamble between paying the premium and the likelihood of needing to make a claim. Depending on the age of the property, unexpected repairs could soon eat into any potential profits; a new boiler, roof, damp courses - these unforeseen issues can cost thousands to repair.

The UK is focused on improving the energy efficiency of houses being built and sold, and it is unclear what legislation may lie in store for homeowners in the future. This could impact landlords just as easily, who could be responsible for ensuring their properties meet increasingly high standards.

Some landlords enjoy taking a hands-on approach to the management of the property. Carrying out inspections, collecting rent, dealing with any issues that might crop up; to some these may be a challenge to relish. For many investors though the day-to-day hassle of managing one, or several, properties is more than they bargained for, or even wanted when investing. If you live far away from your properties, have a troublesome tenant, or part of the property develops an unforeseen problem then this can add additional stress on top of the financial costs.

If you prefer the hands-off approach, then you can always find someone to manage the property for you. They’ll do all the hard work, allowing you to enjoy the rental income. The cost of doing this however is losing a slice of your monthly earnings. Property management fees can range from 5 - 15% of your gross income and there may be other admin fees to set it up.

As the years pass and the property is lived in, it will require further repairs and refurbishments. The general rule is to redecorate and refurbish every ten years in order to keep the property in good condition. The downside, aside from the expenditure, is that every month the property sits empty is a month you might be paying mortgage, insurance and agent fees without earning a single penny.

The same loss of earnings is risked depending on the type of tenants you accept into your property too. Many do not accept students due to the term-time occupation of these houses or flats and the downtime in the summer when the property is not occupied, but many do on the basis that there is a high demand for student accommodation. This is another balancing act for you, the investor, to weigh up.

Rental Income Taxation

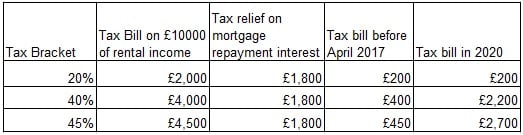

Prior to April 2017, landlords enjoyed a certain amount of tax relief on their rental income. Any interest paid on a buy-to-let mortgage could be deducted from the rental income before it was taxed.

Since April 2017 however, new regulations mean that this tax relief is being reduced slowly. By 2020, landlords will be expected to pay tax on all rental income with a flat tax relief of 20% on the total bill. If you’re earning £10,000 a year in rent, and are paying £9,000 of mortgage interest payments, then you will still be taxed on all £10,000 of the rent.

As you can see from the table below, this can have a significant impact on the tax you will be paying from 2020 onwards.

If declaring your rental income means you will be taxed on a higher bracket, this will also have an impact on all your earnings. This should be taken into serious consideration before purchasing any buy-to-let property. Changing tax brackets applies to you and not just the property in question.

Selling your property

There may come a time when you wish to sell your property, whether because house prices are at a high point, the market is suggesting an imminent price drop, or you might simply wish to release the equity for some other use.

After all the costs of purchasing and maintaining your property you now face further expense in selling it…

Property price

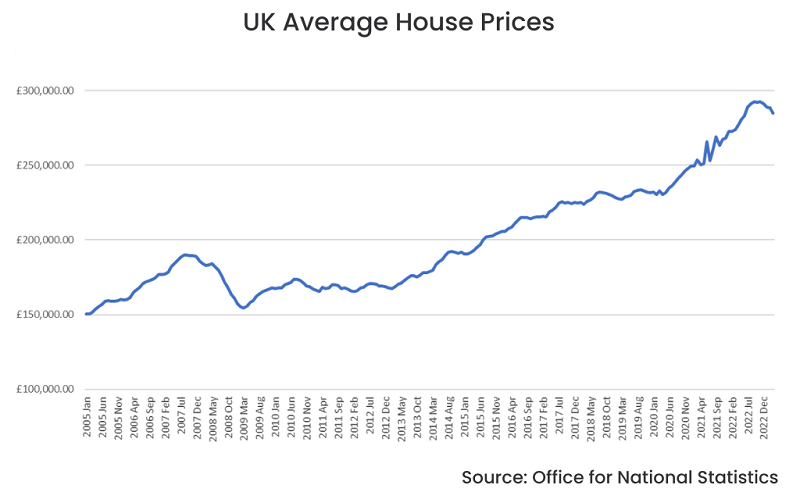

One of the biggest factors to consider is the price you can get when selling the property. The house price market historically has performed well since 2009, but as seen in the chart below there are certainly risks that the price could be lower than when you purchased it.

Since 2005, average house prices have almost doubled from £150,000 to £300,000. In the same period the value of gold has increased more than six times, from £225 per ounce to more than £1,500 per ounce at the time of writing. Although this doesn't take into account potential rental income that could have been earned, it does warrant consideration; significantly higher gains would have been made in the value of gold, without any of the stress or hassle of owning a property.

On the plus side for property investors, demand is high. House building has been slow and with an ever-increasing population the need for housing keeps rising. This has been a large driving force behind the growth in the market up to now.

The current economic climate however is uncertain and looks unfavourable to property in particular. High inflation and rising interest rates have created a perfect storm of a cost-of-living crisis, as well as a potential crash in house prices. With people’s incomes squeezed, many are downsizing or putting off house buying. Refinancing mortgages is expected to see a wave of people selling or struggling to make payments that could result in repossession by banks.

House prices have already started to fall, and this is expected to only worsen throughout 2023 and into 2024. Analysts are unsure how far house prices will fall; demand is still high and supply still low, but both could flip quite quickly if mortgage rates rise as high as expected. Whether a full-blown crash or a long-term slump, people buying a property in the current climate could see their investment value fall in the near-term.

Cost of selling

Assuming you’re happy to sell your property then once again you’re faced with several additional costs. Estate agents and legal fees will eat into your profit margin, and you may need to refurbish once again in order to sell, but CGT is likely to be the biggest cost of all.

Capital Gains Tax – CGT – is a tax paid on the profit made from the sale of an asset. For properties that are not your main home, CGT will be charged on your profit from the sale. If you had purchased a rental property at £200,000, and sold it at £250,000 then the £50,000 profit would be subject to CGT, at a rate up to 28%. There is a tax-free allowance set each year (£6,000 for 2023/24) for CGT, which may be deducted from the profit, but only subject to certain conditions. For more information on CGT we recommend reading the official information provided by the government.

Considering that the house price may have increased in value due to inflation, rather than improvements made by yourself, paying CGT may be a tough pill to swallow for a serious investor, and with CGT thresholds falling further in the coming financial years this tax could be a significant loss to any potential profit you made.

Gold vs property

As an alternative form of investment, gold offers many benefits over buy-to-let properties. The most obvious one is that you can’t sell part of a property, but you can sell some of your gold bullion. Many investors choose a variety of bars and coins as a way of giving themselves flexibility with their asset. Gold is also a very simple investment compared to a buy-to-let property; it is purchased quickly and can be simply stored away without any of the maintenance costs and hassle of a property.

The entry cost for gold is considerably lower, to the point that it can be purchased within a few minutes simply by ordering online like any other commercial product. The initial costs are also far less, and at BullionByPost we sell our gold at an average of 5-8% above the spot price. When you wish to sell, private buyers or dealers like us will be happy to do so at competitive rates, and sales can be completed within a matter of days.

Your asset will not be subject to the same risks as the housing market, and trends show the price of gold is rising independently of other market influences. When you decide you want to sell this can also be done simply and quickly. If your investment is of qualifying types of gold then it will be exempt from both VAT when purchasing and CGT when selling, maximising your profits. We buy back gold at 96% of the market value.

The decision on where to invest your money should always be made after careful consideration of all available information and options. Financial data and regulations change regularly so be sure to check for the latest information.

- Home

- How to Buy?

- Payment Options

- Delivery Options

- Gold Storage

- Storage at Brink's

- Gold Investment Guide

- Why buy gold?

- Is gold a good investment?

- Why Physical Gold?

- Best Time to Buy Gold

- Gold Bars vs Coins?

- Gold vs Silver

- Gold - Silver Ratio explained

- VAT on bullion

- Capital Gains Tax & Gold Bullion

- UK Legal Tender Coins

- Top 5 Gold Investments

- Top 5 Silver Investments

- Gold vs ISAs

- Gold vs Buy-to-Let

- Gold vs FTSE 100

- Gold vs Bitcoin

- Where to buy gold?

- Why buy from us?

- Where to sell gold?

- Coin Shops

- Gold Price Forecasts

- Top 10 Gold Producers

- Top 10 Gold Reserves

- Gold Britannia vs Sovereign

- Britannia coin designs

- Sovereign coin designs

- Sovereign Mintages

- Sovereign mint marks

- British coin specs

- What is a proof coin?

- Royal Mint bullion

- The Queen's Beasts

- Bullion Refiners

- British coin mints

- Gold Tola - India & Pakistan

- Bullion Index

-

- CGT-Free Gold Coins

- 0.5g Gold Coin

- 1oz Gold Coins

- 1/2oz Gold Coins

- 1/4oz Gold Coins

- 1/10oz Gold Coins

- 2026 Gold Coins

- 2025 Gold Coins

-

-

- Charles III Gold Sovereign Coins

- Elizabeth II Fifth Head 2016 - 2022

- Elizabeth II Fourth Head 1998 - 2015

- Elizabeth II Decimal Head 1974 - 1984

- Elizabeth II Young Head 1957-1968

- George V 1911 - 1932

- Edward VII Gold Sovereign Coins 1902 - 1910

- Victoria Old Head 1893 - 1901

- Victoria Jubilee Head 1887 - 1893

- Victoria Young Head Sovereign

- Gold Double Sovereign

- Gold Quintuple Sovereign

-

-

Show More Show Less

-

-

- Half Sovereign Elizabeth II Fifth Head 2016 - 2022

- Half Sovereign Elizabeth II Fourth Head 1998 - 2015

- Half Sovereign Elizabeth II Decimal Head 1980 - 1984

- Half Sovereign George V 1911 - 1926

- Half Sovereign Edward VII 1902-1910

- Half Sovereign Victoria Old Head 1893 - 1901

- Half Sovereign Victoria Jubilee Head 1887 - 1893

- Half Sovereign Victoria Young Head Shield Back 1838 - 1887

- Half Sovereign George IV Bare Head 1826 - 1828

- Half Sovereign George III 1817 - 1820

-

Show More Show Less

-

- Gold Quarter Sovereign

- American Gold Buffalo

- Gold Tudor Beasts

- Royal Mint Gold Myths & Legends

- The Lion and The Eagle Gold Coins

- St George and the Dragon Gold Coins

- Royal Arms Gold Coins

- Six Decades of 007 James Bond Gold Coins

- Gold Queen's Beasts

- Royal Mint Gold Lunar

- Best Value Gold Coins 1oz

-

- Andorran Coins

- Australian Gold Coins

- Austrian Gold Coins

- British Gold Coins

- Bahamas Coins

- Bahrain Coins

- Belgian Gold Coins

- Botswanan Gold Coins

- Burundi Coins

-

Show More Show Less

- Canadian Gold Coins

- Chilean Gold Coins

- Costa Rican Coins

- Cuban Gold Coins

- Cyprus Gold Coins

- Danish Gold Coins

- Dutch Gold Coins

- Fiji Coins

- Gambian Coins

- German Gold Coins

- Hong Kong Gold Coins

- Hungarian Gold Coins

- Indian Coins

- Irish Gold Coins

- Isle of Man Gold Coins

- Israeli Gold Coins

- Italian Gold Coins

- Jamaican Gold Coins

- Jordanian Coins

- Latvian Coins

- Lesotho Gold Coins

- Macau Coins

- Malaysia Coins

- Maltese Gold Coins

- Mauritian Coins

- Mexican Gold Coins

- Nepalese Coins

- New Zealand Gold Coins

- Pakistani Coins

- Persian Gold Coins

- Peruvian Gold Coins

- Rwanda Gold Coins

- Sardinia Gold Coins

- Saudi Arabian Coins

- Scottish Gold Coins

- Singapore Gold Coins

- Somalian Gold Coins

- South African Gold Coins

- Spanish Gold Coins

- St Helena Gold Coins

- Sudanese Coins

- Swedish Kronor

- Swiss Gold Coins

- Tanzanian Coins

- Thai Coins

- Tonga Coins

- Tunisian Coins

- Turkish Gold Coins

- United Arab Emirates Gold Coins

- Uruguay Gold Coins

- Venezuelan Coins

- Colombian Gold Coins

- Isle of Man Angel

- Isle of Man Gold Noble

- Isle of Man Sovereign

- Somalian African Wildlife Gold Coins

- South African Big Five Series

- 22k Gold Coins

- 24k Gold Coins

- Perth Mint Gold Wildlife Coins

-

-

- CGT-Free Silver Coins

- 1oz Silver Coins

- 2026 Silver Coins

- 2025 Silver Coins

- Silver Coin Sets

- 2oz Silver Coins

- 5oz Silver Coins

- 10oz Silver Coins

- Silver Canadian Maple

-

Show More Show Less

- Austrian Silver Philharmonic

- Perth Mint Silver Lunar Series

- American Eagle

- The Lion and The Eagle Silver Coins

- Royal Mint Silver Myths & Legends

- St George and the Dragon Silver Coins

- Silver Krugerrand

- Chinese Panda

- Australian Silver Kangaroo

- Australian Koala

- Australian Quokka

- Australian Silver Kookaburra

- Australian Silver Brumby

- Australian Silver Wedge Tailed Eagle

- Australian Wombat

- Australian Silver Swan

- Australian Emu

- Silver Armenian Noah's Ark

- Silver Trees of Life Rounds

- Silver Tudor Beasts

- Silver Royal Arms

- Six Decades of 007 James Bond Silver Coins

- Egyptian Relic Series

- Star Wars Silver Coins

- Silver Queen's Beasts

- Marvel Series Superhero Coins

- DC Comics Series Superhero Coins

- Isle of Man Silver Angel

- Rwanda African Ounce

- Czech Lion Silver Coins

- Somalian African Wildlife Silver Coins

- Slovakian Eagle Silver Coins

- Australian Mint Silver Coins

- Isle of Man Silver Noble

- Komodo Dragon

- Mexican Libertad

- Dragon Rectangle Coin

- 1 Kilo Silver Coins

- Pre-Owned Silver Coins

- Pre 1947 British Silver Coins (.500)

- Sterling Silver Coins (.925)

- Silver Proof Coins & Sets

-

-

-

- King Charles III Proof Coronation Coins

- King Charles III 75th Birthday Proof Coins

- Queen Elizabeth II Memorial Proof Coins

- Royal Mint Annual Commemorative Sets

- Royal Mint Lunar Proof Coins

- Music Legends Proof Coins

- Winnie the Pooh and Friends Proof Coins

- Royal Mint Harry Potter Proof Coins

- Royal Mint Star Wars Proof Coins

- The Snowman Proof Coins

- Krugerrand Proof Coins

-

- Platinum Proof Coins and Sets

- Royal Mint 1/4oz Proof Coins

- Royal Mint 1oz Gold Proof Coins

- Proof £2 coins

- Proof £5 coins

-

Show More Show Less

-

-

- Charles I Coins

- Charles II Coins

- Edward I Coins

- Edward II Coins

- Edward III Coins

- Edward IV Coins

- Edward the Confessor

- Edward VI Coins

- Edward VII Coins

- Elizabeth I Coins

-

Show More Show Less

- Elizabeth II Coins

- Ethelred the Unready

- George I Coins

- George II Coins

- George III Coins

- George IV Coins

- George V Coins

- George VI Coins

- Harthacnut Coins

- Henry II Coins

- Henry III Coins

- Henry IV Coins

- Henry V Coins

- Henry VI Coins

- Henry VII Coins

- Henry VIII Coins

- James I Coins

- James II Coins

- King Cnut Coins

- King John Coins

- Oliver Cromwell Coins

- Philip and Mary Coins

- Queen Anne Coins

- Queen Victoria Coins

- Richard I Coins

- Richard II Coins

- William and Mary Coins

- William III Coins

- William IV Coins

- William the Conqueror

- Graded Coins

-

-

- Request an Information Pack

- Sign up to our Newsletter