Rated Excellent on Trustpilot

Rated Excellent on Trustpilot

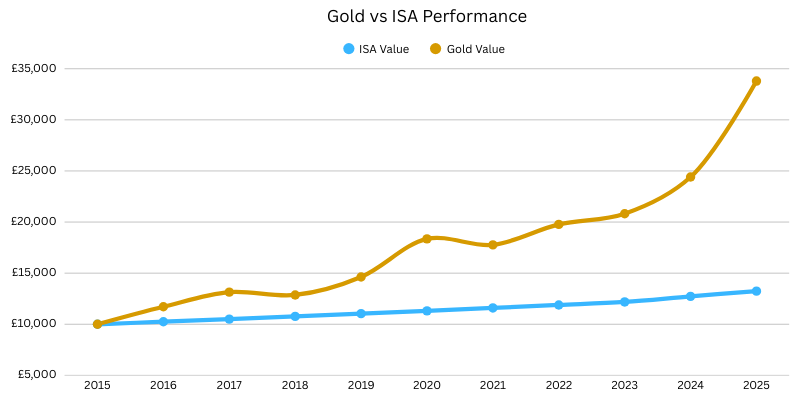

Gold vs ISAs

Register

Register for a free account to buy online, monitor your orders, and receive thoughtful commentary on gold and silver alongside updates on newly released products.

Register Now

ISAs vs Gold: Which works harder for you?

Its important to weigh up the options with your own research, with a lot of investment options offering their own compelling arguments. That said, gold is often referred to a being a "safe haven" with regards to long term preservation of wealth when taking into account things like inflation. And with markets and political volatility, precious metals is often considered as a viable option when people consider where to invest.

The graph below shows the performance of £10,000 between 2015 and 2025 in gold, compared to the same investment into a Cash ISA. For the ISA we have used typical fixed ISA rates available in those time periods (ranging from 2.5% to 4.5%). Gold value has been calculated using gold spot price percentage changes. View our CGT Free Gold Coins.

The takeaway: Gold or ISA?

But if you want clarity, control, and a hedge against inflation, gold continues to be a strong option. In a world of shrinking ISA allowances and shifting rules, many investors prefer a store of value they can hold, and rely on, in any economic climate.

Learn more by visiting out knowledge base.

Shop our CGT Free Gold Coins:

from £256.00

from £357.90

from £752.20

from £379.80

- Home

- How to Buy?

- Payment Options

- Delivery Options

- Gold Storage

- Storage at Brink's

- Gold Investment Guide

- Why buy gold?

- Is gold a good investment?

- Why Physical Gold?

- Best Time to Buy Gold

- Gold Bars vs Coins?

- Gold vs Silver

- Gold - Silver Ratio explained

- VAT on bullion

- Capital Gains Tax & Gold Bullion

- UK Legal Tender Coins

- Top 5 Gold Investments

- Top 5 Silver Investments

- Gold vs ISAs

- Gold vs Buy-to-Let

- Gold vs FTSE 100

- Gold vs Bitcoin

- Where to buy gold?

- Why buy from us?

- Where to sell gold?

- Coin Shops

- Gold Price Forecasts

- Top 10 Gold Producers

- Top 10 Gold Reserves

- Gold Britannia vs Sovereign

- Britannia coin designs

- Sovereign coin designs

- Sovereign Mintages

- Sovereign mint marks

- British coin specs

- What is a proof coin?

- Royal Mint bullion

- The Queen's Beasts

- Bullion Refiners

- British coin mints

- Gold Tola - India & Pakistan

- Bullion Index

-

- CGT-Free Gold Coins

- 0.5g Gold Coin

- 1oz Gold Coins

- 1/2oz Gold Coins

- 1/4oz Gold Coins

- 1/10oz Gold Coins

- 2026 Gold Coins

- 2025 Gold Coins

-

-

- Charles III Gold Sovereign Coins

- Elizabeth II Fifth Head 2016 - 2022

- Elizabeth II Fourth Head 1998 - 2015

- Elizabeth II Decimal Head 1974 - 1984

- Elizabeth II Young Head 1957-1968

- George V 1911 - 1932

- Edward VII Gold Sovereign Coins 1902 - 1910

- Victoria Old Head 1893 - 1901

- Victoria Jubilee Head 1887 - 1893

- Victoria Young Head Sovereign

- Gold Double Sovereign

- Gold Quintuple Sovereign

-

-

Show More Show Less

-

-

- Half Sovereign Elizabeth II Fifth Head 2016 - 2022

- Half Sovereign Elizabeth II Fourth Head 1998 - 2015

- Half Sovereign Elizabeth II Decimal Head 1980 - 1984

- Half Sovereign George V 1911 - 1926

- Half Sovereign Edward VII 1902-1910

- Half Sovereign Victoria Old Head 1893 - 1901

- Half Sovereign Victoria Jubilee Head 1887 - 1893

- Half Sovereign Victoria Young Head Shield Back 1838 - 1887

- Half Sovereign George IV Bare Head 1826 - 1828

- Half Sovereign George III 1817 - 1820

-

Show More Show Less

-

- Gold Quarter Sovereign

- American Gold Buffalo

- Gold Tudor Beasts

- Royal Mint Gold Myths & Legends

- The Lion and The Eagle Gold Coins

- St George and the Dragon Gold Coins

- Royal Arms Gold Coins

- Six Decades of 007 James Bond Gold Coins

- Gold Queen's Beasts

- Royal Mint Gold Lunar

- Best Value Gold Coins 1oz

-

- Andorran Coins

- Australian Gold Coins

- Austrian Gold Coins

- British Gold Coins

- Bahamas Coins

- Bahrain Coins

- Belgian Gold Coins

- Botswanan Gold Coins

- Burundi Coins

-

Show More Show Less

- Canadian Gold Coins

- Chilean Gold Coins

- Costa Rican Coins

- Cuban Gold Coins

- Cyprus Gold Coins

- Danish Gold Coins

- Dutch Gold Coins

- Fiji Coins

- Gambian Coins

- German Gold Coins

- Hong Kong Gold Coins

- Hungarian Gold Coins

- Indian Coins

- Irish Gold Coins

- Isle of Man Gold Coins

- Israeli Gold Coins

- Italian Gold Coins

- Jamaican Gold Coins

- Jordanian Coins

- Latvian Coins

- Lesotho Gold Coins

- Macau Coins

- Malaysia Coins

- Maltese Gold Coins

- Mauritian Coins

- Mexican Gold Coins

- Nepalese Coins

- New Zealand Gold Coins

- Pakistani Coins

- Persian Gold Coins

- Peruvian Gold Coins

- Rwanda Gold Coins

- Sardinia Gold Coins

- Saudi Arabian Coins

- Scottish Gold Coins

- Singapore Gold Coins

- Somalian Gold Coins

- South African Gold Coins

- Spanish Gold Coins

- St Helena Gold Coins

- Sudanese Coins

- Swedish Kronor

- Swiss Gold Coins

- Tanzanian Coins

- Thai Coins

- Tonga Coins

- Tunisian Coins

- Turkish Gold Coins

- United Arab Emirates Gold Coins

- Uruguay Gold Coins

- Venezuelan Coins

- Colombian Gold Coins

- Isle of Man Angel

- Isle of Man Gold Noble

- Isle of Man Sovereign

- Somalian African Wildlife Gold Coins

- South African Big Five Series

- 22k Gold Coins

- 24k Gold Coins

- Perth Mint Gold Wildlife Coins

-

-

- CGT-Free Silver Coins

- 1oz Silver Coins

- 2026 Silver Coins

- 2025 Silver Coins

- Silver Coin Sets

- 2oz Silver Coins

- 5oz Silver Coins

- 10oz Silver Coins

- Silver Canadian Maple

-

Show More Show Less

- Austrian Silver Philharmonic

- Perth Mint Silver Lunar Series

- American Eagle

- The Lion and The Eagle Silver Coins

- Royal Mint Silver Myths & Legends

- St George and the Dragon Silver Coins

- Silver Krugerrand

- Chinese Panda

- Australian Silver Kangaroo

- Australian Koala

- Australian Quokka

- Australian Silver Kookaburra

- Australian Silver Brumby

- Australian Silver Wedge Tailed Eagle

- Australian Wombat

- Australian Silver Swan

- Australian Emu

- Silver Armenian Noah's Ark

- Silver Trees of Life Rounds

- Silver Tudor Beasts

- Silver Royal Arms

- Six Decades of 007 James Bond Silver Coins

- Egyptian Relic Series

- Star Wars Silver Coins

- Silver Queen's Beasts

- Marvel Series Superhero Coins

- DC Comics Series Superhero Coins

- Isle of Man Silver Angel

- Rwanda African Ounce

- Czech Lion Silver Coins

- Somalian African Wildlife Silver Coins

- Slovakian Eagle Silver Coins

- Australian Mint Silver Coins

- Isle of Man Silver Noble

- Komodo Dragon

- Mexican Libertad

- Dragon Rectangle Coin

- 1 Kilo Silver Coins

- Pre-Owned Silver Coins

- Pre 1947 British Silver Coins (.500)

- Sterling Silver Coins (.925)

- Silver Proof Coins & Sets

-

-

-

- King Charles III Proof Coronation Coins

- King Charles III 75th Birthday Proof Coins

- Queen Elizabeth II Memorial Proof Coins

- Royal Mint Annual Commemorative Sets

- Royal Mint Lunar Proof Coins

- Music Legends Proof Coins

- Winnie the Pooh and Friends Proof Coins

- Royal Mint Harry Potter Proof Coins

- Royal Mint Star Wars Proof Coins

- The Snowman Proof Coins

- Krugerrand Proof Coins

-

- Platinum Proof Coins and Sets

- Royal Mint 1/4oz Proof Coins

- Royal Mint 1oz Gold Proof Coins

- Proof £2 coins

- Proof £5 coins

-

Show More Show Less

-

-

- Charles I Coins

- Charles II Coins

- Edward I Coins

- Edward II Coins

- Edward III Coins

- Edward IV Coins

- Edward the Confessor

- Edward VI Coins

- Edward VII Coins

- Elizabeth I Coins

-

Show More Show Less

- Elizabeth II Coins

- Ethelred the Unready

- George I Coins

- George II Coins

- George III Coins

- George IV Coins

- George V Coins

- George VI Coins

- Harthacnut Coins

- Henry II Coins

- Henry III Coins

- Henry IV Coins

- Henry V Coins

- Henry VI Coins

- Henry VII Coins

- Henry VIII Coins

- James I Coins

- James II Coins

- King Cnut Coins

- King John Coins

- Oliver Cromwell Coins

- Philip and Mary Coins

- Queen Anne Coins

- Queen Victoria Coins

- Richard I Coins

- Richard II Coins

- William and Mary Coins

- William III Coins

- William IV Coins

- William the Conqueror

- Graded Coins

-

-

- Request an Information Pack

- Sign up to our Newsletter